Compliance

Customers don't need to clear documents through internal review or negotiate confidentiality before running an analysis.

A multi-agent system, engineered around twenty years of merger enforcement experience, that produces a complete antitrust analysis in 10 to 25 minutes.

Taimet isn't a wrapper around a chatbot. It's a proprietary pipeline of more than a hundred coordinated AI tasks, drawing on multiple LLM providers, verifying its own work, and reasoning the way a senior antitrust attorney actually reasons.

A typical Taimet analysis runs more than a hundred coordinated LLM responses across multiple providers. Some agents research; some reason; some synthesize; some verify. They run in parallel where speed matters and in sequence where one stage depends on the output of another.

The system spawns additional agents on the fly when a transaction calls for deeper investigation - more agents for a deal with significant vertical exposure, more agents for a transaction spanning many product or geographic markets.

The result is research and analysis that would take a senior antitrust attorney days, delivered end-to-end in 10 to 25 minutes.

Proprietary Architecture

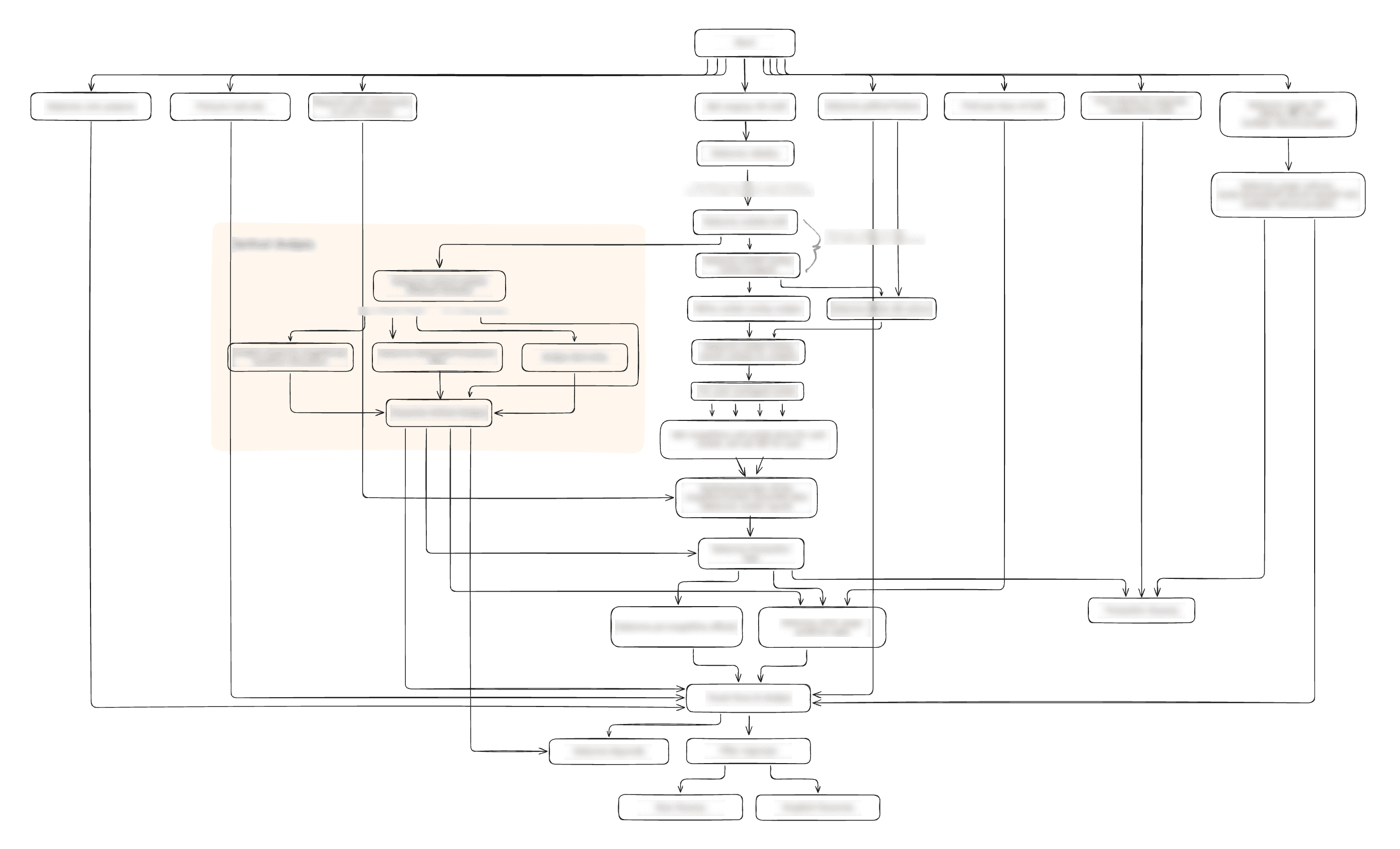

Why we show it. In a world full of AI tools, it’s reasonable to wonder whether there’s real engineering behind the curtain or just a clever prompt. This diagram is the first part of our answer. The AI does what it's good at, but it runs inside a purpose-built architecture that controls what gets asked, in what order, how results are verified, and how everything fits together. This structure is why Taimet produces defensible analysis instead of plausible-sounding text.

This diagram is based on our internal workflow spec: the same blueprint we use to run live analyses. Details are blurred, but each box represents a step in our custom-made system. Many of those steps are entire sub-systems in their own right.

This is what “more than one hundred tasks” really means in practice: complex research, analysis, verification, and synthesis.

Most AI tools force a tradeoff: either rigid, scripted workflows that can't adapt, or open-ended LLM calls that drift, hallucinate, and resist verification. Taimet refuses the tradeoff.

Inside the pipeline, agents reason the way a skilled human researcher does - forming hypotheses, exploring them, updating their conclusions as new evidence comes in. But at defined checkpoints, the system extracts that reasoning into structured, deterministic data: identified markets, calculated HHI, vertical relationships. Those structures are what feed the next stage of analysis, get displayed in the report, and make every conclusion auditable.

Hypothesis generation, market definition, qualitative reasoning, and synthesis - work that requires judgment, not rules.

Market lists, HHI, score components, citations, and report sections - outputs that need to be parseable, verifiable, and consistent.

Every Taimet analysis is built from public information. We start with the highest-quality primary sources - SEC filings, investor presentations, court records, regulatory filings - and layer in reputable news, trade publications, press releases, and other public materials.

This isn't a stylistic choice. It's a foundational decision with direct consequences for our customers:

Because every conclusion is grounded in public data, investors trading on Taimet's analysis don't carry insider-trading risk from the analysis itself.

No confidentiality negotiations, no protective orders. The analysis arrives in 30 minutes, not 30 days.

Sources are cited throughout. Every source is checkable. The reasoning is auditable from end to end.

Hallucination is the central problem with using general-purpose LLMs for high-stakes legal and economic analysis. The errors sound plausible. They're hard for a human reviewer to catch. And once a wrong claim enters the pipeline, downstream analysis builds on top of it.

Taimet addresses this with verification passes throughout the analysis. Citation-checking agents confirm that claims are actually supported by the cited sources. Reasoning-consistency checks compare conclusions across agents. Claims without source support are flagged. Different stages of the pipeline cross-validate each other before the report is finalized.

What separates Taimet from a generic AI tool isn't the AI - it's the prompting layer. Hundreds of pages of carefully crafted prompts encode how Gwendolyn Lindsay Cooley, Taimet's founder and a 19-year Assistant Attorney General for Antitrust, actually reasons through a merger.

We built it the slow way. For each step a human antitrust attorney would take, Gwendolyn walked through her reasoning in detail. We interrogated every choice - why this market definition and not another, why this factor matters in this industry, why would a state attorney general care about this kind of deal - until the reasoning was explicit. Then we wrote it into the system.

Small-molecule drugs are in the same market only if they share an identical molecular structure and are AB-rated for each other. Biologics are in the same market only if they’re biosimilars and treat the same disease. The distinction determines whether a pharma deal looks like a horizontal overlap or a non-issue. Most analysts don’t know it. Taimet does - and applies it automatically.

Different state attorneys general challenge different kinds of mergers. Some are aggressive on hospital consolidation. Others on agriculture. Others on tech. Taimet knows which jurisdictions are likely to act on which transactions, which state-level enforcement theories apply, and which mergers will draw multistate coalitions.

Pricing-power evidence often surfaces in investor presentations. Foreclosure intent shows up in board materials. Public statements about competitive intent surface in regulatory filings before they show up in press releases. Taimet knows where to look - because the person who designed it spent two decades looking there.

Taimet identifies the transaction structure automatically - horizontal, vertical, conglomerate, cross-market, cluster market, private equity, or any combination. Most real deals involve more than one structure at once. A private equity roll-up in a health services market may face horizontal overlap, vertical foreclosure concerns, and cumulative competition effects simultaneously. The system applies the right analytical frameworks for each without the user needing to classify the deal first.

Companies with overlap in both product and geographic market, competing directly in the same space.

Companies in a direct or indirect vertical relationship within the same supply chain.

An acquisition in an unrelated industry, with no economic relationship between the companies.

Multiple products sold together as a bundle (e.g., supermarket goods, hospital services).

Companies selling identical products but operating in separate, non-overlapping geographic markets.

A private equity firm acquiring a company in a market where it has no existing holdings.

Across every industry

Both federal agencies build their enforcement staffs around industry teams. A human analyst has to choose what to know deeply. That structural constraint doesn't apply to Taimet. The same system that analyzes a pharmaceutical merger - where market definition turns on molecular structure and AB-rating - analyzes a semiconductor deal, a regional hospital consolidation, or a mining joint venture. No configuration required. For the first time, the analytical breadth of the entire merger landscape is available to a single analyst.

Every analysis produces a 0-100 Taimet Score™, mapped to six interpretive bands. The bands are designed to reflect the actual range of merger outcomes - from quick clearance through trial on the merits to adverse decision - as an experienced attorney would predict them.

Score Ranges

1–25Early termination

Parties may be granted early termination of the HSR waiting period when the transaction is unlikely to substantially lessen competition.

26–50Pull and refile

The merging parties can withdraw and refile to give enforcers more time, so review often extends beyond the usual 30-day window.

51–70Second request

These deals carry a higher risk of a second request and a longer review; toward the top of the band, negotiated outcomes become more common.

71–85Remedies

A complaint and structural or behavioral remedies are plausible, with lower scores leaning toward settlement and higher scores toward litigation.

86–95Trial on the merits

Substantial antitrust effects with few likely remedies can produce a litigated trial on the merits.

96–100Adverse decision

Strong anticompetitive concerns and limited remedies may lead to trial and an adverse decision against the merging parties.

1 to 25, Early termination: Parties may be granted early termination of the HSR waiting period when the transaction is unlikely to substantially lessen competition. 26 to 50, Pull and refile: The merging parties can withdraw and refile to give enforcers more time, so review often extends beyond the usual 30-day window. 51 to 70, Second request: These deals carry a higher risk of a second request and a longer review; toward the top of the band, negotiated outcomes become more common. 71 to 85, Remedies: A complaint and structural or behavioral remedies are plausible, with lower scores leaning toward settlement and higher scores toward litigation. 86 to 95, Trial on the merits: Substantial antitrust effects with few likely remedies can produce a litigated trial on the merits. 96 to 100, Adverse decision: Strong anticompetitive concerns and limited remedies may lead to trial and an adverse decision against the merging parties.

Taimet was designed first as an initial screening tool. For enforcers, it shows where to focus and what to set aside. For investors, it surfaces risk the market may not have priced in. For law firms, it produces market-overlap research that would otherwise take days.

But Taimet stops where human judgment begins. The system is built to assist expert judgment, not replace it - and every output is designed to be reviewed, challenged, and built upon by the human in the loop.

Taimet doesn't accept uploads. We don't process party-supplied documents. We don't ingest deal materials. To run an analysis, the system needs only the names of the merging companies. This serves three purposes at once:

Customers don't need to clear documents through internal review or negotiate confidentiality before running an analysis.

No party-confidential data ever enters the system, which means none can leak from it.

Taimet can't be used as a sandbox to reverse-engineer which factors lower a score. The integrity of the analysis can't be manipulated.

Watch our walkthrough of Taimet's key features and the resulting analysis.

What happens next