Compliance

Customers don't need to clear documents through internal review or negotiate confidentiality before running an analysis.

For investment firms

Taimet is purpose-built for merger antitrust risk. A full analysis in minutes built exclusively with public data and cited sources your team can check before the next call.

The core question is not "Is there regulatory risk?" It is "what will regulators actually do?" Early termination, second request, or remedies? The answer determines whether the spread compresses or widens. Manual research takes a day or more to approach that question. And you'll still call your go-to attorney for confirmation. General-purpose LLMs are faster, but confidently wrong on antitrust in ways experts can catch and non-experts cannot: wrong guidelines, fabricated citations, vague industry positions that sound right but are not.

Taimet is built to answer the outcome question directly: a full antitrust read in 10-25 minutes, scored against six real-world regulatory outcome bands - from early termination through remedies to adverse decision - with exclusively public data and cited sources.

Expert-grade antitrust with public data - at market speed, with sources that hold up.

Taimet surfaces relevant product and geographic markets - including overlaps that are not obvious from headlines or initial coverage. You get the full picture, with cited sources, early enough to act on it.

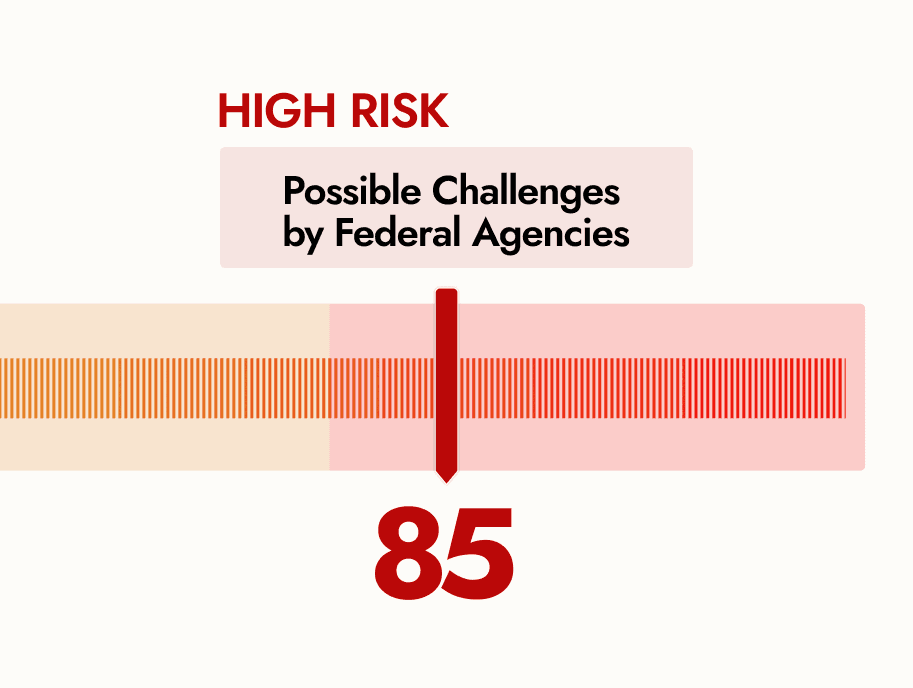

The Taimet Score™ maps to six real-world outcome bands - early termination, pull and refile, second request, remedies, trial on the merits, adverse decision - representing what federal and state enforcers are likely to do. These are not abstract risk levels; they are outcome predictions. A score in the 51-70 band means a second request is possible. 71-85 puts the deal in remedies territory. A full written report sits behind every score.

You already have the right instinct. The value is in pressure-testing its edges. Taimet surfaces enforcement posture, state AG alignment, and less-visible vertical exposure that don't appear on a first pass. The score isn't there to validate - it's there to sharpen. And the delta is where conviction becomes precision.

Traditional analysis depends heavily on which lawyer or analyst you ask. Taimet standardizes the framework, so investors can compare deals apples-to-apples across sectors and time.

Every material claim traces to a public source. When Taimet's read departs from your thesis, the citation trail tells you exactly where to look. It confirms when you are right and surfaces exactly where your hypothesis needs reexamining.

Taimet is built with public records, SEC filings, regulatory documents, and news - never party-supplied materials or confidential information. The analysis itself creates no insider exposure. Work fast on a live deal without that risk.

Every analysis produces a 0-100 Taimet Score™, mapped to six interpretive bands. The bands are designed to reflect the actual range of merger outcomes - from quick clearance through trial on the merits to adverse decision - as an experienced attorney would predict them.

Score Ranges

1–25Early termination

Parties may be granted early termination of the HSR waiting period when the transaction is unlikely to substantially lessen competition.

26–50Pull and refile

The merging parties can withdraw and refile to give enforcers more time, so review often extends beyond the usual 30-day window.

51–70Second request

These deals carry a higher risk of a second request and a longer review; toward the top of the band, negotiated outcomes become more common.

71–85Remedies

A complaint and structural or behavioral remedies are plausible, with lower scores leaning toward settlement and higher scores toward litigation.

86–95Trial on the merits

Substantial antitrust effects with few likely remedies can produce a litigated trial on the merits.

96–100Adverse decision

Strong anticompetitive concerns and limited remedies may lead to trial and an adverse decision against the merging parties.

1 to 25, Early termination: Parties may be granted early termination of the HSR waiting period when the transaction is unlikely to substantially lessen competition. 26 to 50, Pull and refile: The merging parties can withdraw and refile to give enforcers more time, so review often extends beyond the usual 30-day window. 51 to 70, Second request: These deals carry a higher risk of a second request and a longer review; toward the top of the band, negotiated outcomes become more common. 71 to 85, Remedies: A complaint and structural or behavioral remedies are plausible, with lower scores leaning toward settlement and higher scores toward litigation. 86 to 95, Trial on the merits: Substantial antitrust effects with few likely remedies can produce a litigated trial on the merits. 96 to 100, Adverse decision: Strong anticompetitive concerns and limited remedies may lead to trial and an adverse decision against the merging parties.

Taimet's Founder, Gwendolyn Lindsay Cooley, served nearly two decades as Wisconsin's Assistant Attorney General for Antitrust. She chaired the National Association of Attorneys General Multistate Antitrust Task Force, leading coalitions of state and federal enforcers and collaborating with international counterparts. She co-led the trial team for the States' challenge to T-Mobile/Sprint - one of the highest-profile telecom antitrust cases in recent history.

Most AI products are built by AI researchers who consult lawyers. Taimet was built by a lawyer who spent two decades doing this work, in partnership with an engineer with two decades building production software. The reasoning encoded into the system isn't theoretical. It's hers.

Read more about Gwendolyn's background →

There is a small body of working knowledge - the kind held by people who have spent years doing this - that determines how mergers actually get analyzed. None of it is in a textbook. Almost none of it is in an LLM's training data. All of it is in Taimet.

Small-molecule drugs are in the same market only if they share an identical molecular structure and are AB-rated for each other. Biologics are in the same market only if they’re biosimilars and treat the same disease. The distinction determines whether a pharma deal looks like a horizontal overlap or a non-issue. Most analysts don’t know it. Taimet does - and applies it automatically.

Different state attorneys general challenge different kinds of mergers. Some are aggressive on hospital consolidation. Others on agriculture. Others on tech. Taimet knows which jurisdictions are likely to act on which transactions, which state-level enforcement theories apply, and which mergers will draw multistate coalitions.

Pricing-power evidence often surfaces in investor presentations. Foreclosure intent shows up in board materials. Public statements about competitive intent surface in regulatory filings before they show up in press releases. Taimet knows where to look - because the person who designed it spent two decades looking there.

These are three examples among dozens. The full set is what makes the difference between an analysis that sounds expert and one that actually is.

Taimet identifies the transaction structure automatically - horizontal, vertical, conglomerate, cross-market, cluster market, private equity, or any combination. Most real deals involve more than one structure at once. A private equity roll-up in a health services market may face horizontal overlap, vertical foreclosure concerns, and cumulative competition effects simultaneously. The system applies the right analytical frameworks for each without the user needing to classify the deal first.

Companies with overlap in both product and geographic market, competing directly in the same space.

Companies in a direct or indirect vertical relationship within the same supply chain.

An acquisition in an unrelated industry, with no economic relationship between the companies.

Multiple products sold together as a bundle (e.g., supermarket goods, hospital services).

Companies selling identical products but operating in separate, non-overlapping geographic markets.

A private equity firm acquiring a company in a market where it has no existing holdings.

Across every industry

Both federal agencies build their enforcement staffs around industry teams. A human analyst has to choose what to know deeply. That structural constraint doesn't apply to Taimet. The same system that analyzes a pharmaceutical merger - where market definition turns on molecular structure and AB-rating - analyzes a semiconductor deal, a regional hospital consolidation, or a mining joint venture. No configuration required. For the first time, the analytical breadth of the entire merger landscape is available to a single analyst.

Taimet was designed first as an initial screening tool. It surfaces regulatory risk the market may not have priced in - markets, overlaps, vertical exposure, enforcement context - in 10-25 minutes, so your team can test a thesis or identify blind spots before the next call.

But Taimet stops where human judgment begins. Investors still corroborate the market data. Portfolio managers still size the position. The system is built to sharpen expert judgment, not replace it - and every output is designed to be reviewed, challenged, and built upon by the human in the loop.

Taimet doesn't accept uploads. We don't process party-supplied documents. We don't ingest deal materials. To run an analysis, the system needs only the names of the merging companies. This serves three purposes at once:

Customers don't need to clear documents through internal review or negotiate confidentiality before running an analysis.

No party-confidential data ever enters the system, which means none can leak from it.

Taimet can't be used as a sandbox to reverse-engineer which factors lower a score. The integrity of the analysis can't be manipulated.

Hallucination is the central problem with using general-purpose LLMs for high-stakes legal and economic analysis. The errors sound plausible. They're hard for a human reviewer to catch. And once a wrong claim enters the pipeline, downstream analysis builds on top of it.

Taimet addresses this with verification passes throughout the analysis. Citation-checking agents confirm that claims are actually supported by the cited sources. Reasoning-consistency checks compare conclusions across agents. Claims without source support are flagged. Different stages of the pipeline cross-validate each other before the report is finalized.

“When you are reviewing multiple transactions with a small team, the constraint isn't judgment, it's time. A tool like this does not replace discretion, but it immediately shows you where to focus it.”

“Reflecting the creator's experience of regulatory matters, the depth of analysis, and more importantly the consistency, is far beyond anything we've seen from general tools. It's genuinely useful for investment decisions.”

“Even as antitrust enforcement becomes less predictable, the need for a clear, consistent view of risk hasn't gone away - if anything, it's more important. Taimet is one of the few tools that brings real structure to that uncertainty. We've been early believers, and it's become a critical part of how we advise investors in live situations.”

“Taimet is the first tool I've seen that genuinely closes the gap between legal analysis and investor needs. It delivers clarity where there used to be noise, and it's quickly become indispensable to how we advise our clients.”

For investors